Most companies that use a Balanced Scorecard inherited it. A consultant brought it in, or the CFO read Kaplan and Norton in the 90s and the framework stuck. That's not a criticism — the Balanced Scorecard changed how organisations think about strategy. Before it existed, most companies measured success almost entirely through financial metrics. Revenue, profit, cost. Full stop.

The BSC said: that's not enough. Financial results are lagging indicators. If you want to understand why you're winning or losing, you also need to look at customers, internal processes, and your people.

That insight still holds. What's changed is the pace of business, and the tools available to act on it.

This article walks through what a Balanced Scorecard looks like in practice — with examples across industries — and then gets honest about where the framework struggles and what teams are doing instead.

What is the Balanced Scorecards framework?

The Balanced Scorecard is a strategic management framework developed by Robert Kaplan and David Norton in the early 1990s. It was introduced in a 1992 Harvard Business Review article and remains one of the most widely used tools in the strategic management process.

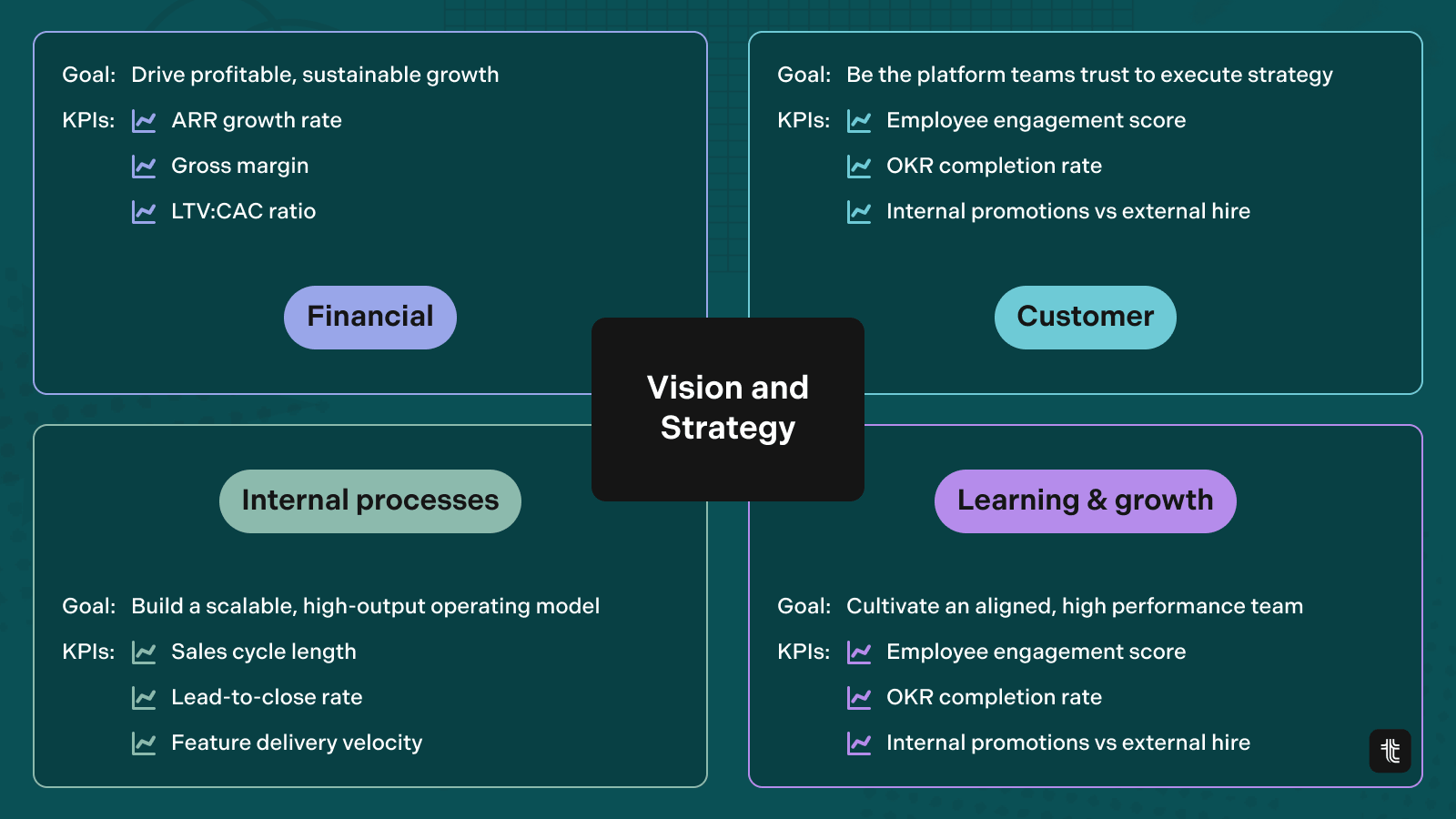

The central idea: measuring performance across four perspectives gives you a more complete picture than financials alone.

The four perspectives are:

- Financial — Are we delivering value to shareholders? (Revenue, profit margin, ROI)

- Customer — How are we seen by our customers? (NPS, retention, satisfaction scores)

- Internal Processes — What must we do well operationally? (Cycle time, quality, throughput)

- Learning and Growth — How do we improve and innovate? (Training, employee satisfaction, capability)

Each perspective includes objectives, measures (KPIs), targets, and initiatives. The idea is that progress in learning and growth drives better internal processes, which improves customer outcomes, which eventually shows up in financial results. It's a cause-and-effect chain.

The Four Perspectives in practice

Here's where most articles stop at theory. Let's look at what these perspectives actually look like when filled in.

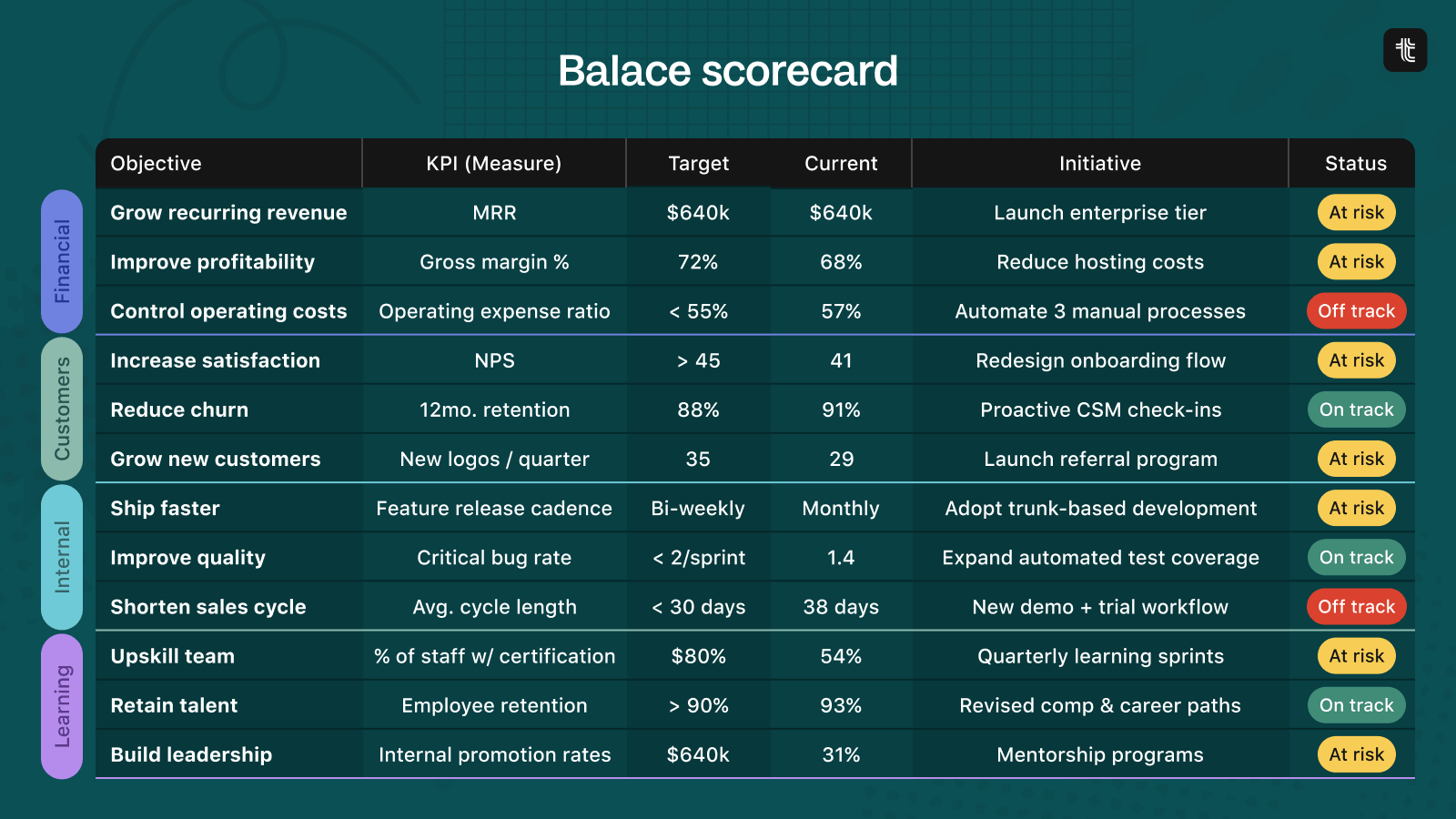

Financial perspective

This is the most intuitive. A company might set:

- Objective: Increase recurring revenue

- Measure: Monthly recurring revenue (MRR)

- Target: 15% growth quarter on quarter

- Initiative: Launch new enterprise tier

Customer perspective

This one trips people up because 'customer satisfaction' can mean many things. In a well-built BSC:

- Objective: Improve customer retention

- Measure: 12-month retention rate, NPS

- Target: NPS above 40, retention above 85%

- Initiative: Launch dedicated onboarding programme

Internal Processes perspective

This is where you track the operational machinery that delivers your customer promise:

- Objective: Reduce time-to-value for new customers

- Measure: Days from sign-up to first successful outcome

- Target: Under 14 days (from current 30)

- Initiative: Redesign onboarding flow; add in-app checklists

Learning and Growth perspective

The hardest to measure, but the one that makes everything else sustainable:

- Objective: Build strategic planning capability across the leadership team

- Measure: % of managers trained on OKR methodology; internal promotion rate

- Target: 80% certified, 40% of senior hires from internal pipeline

- Initiative: Quarterly leadership training series; mentorship programme

Balanced Scorecard examples by industry

Technology / SaaS

A software company might structure its BSC like this:

- Financial: Grow ARR from $5M to $8M; improve gross margin to 75%

- Customer: Reduce churn below 5% annually; NPS above 45

- Internal Processes: Deploy new features bi-weekly; reduce critical bug rate by 50%

- Learning and Growth: Launch engineer development programme; hire 3 senior PMs

The SaaS BSC works well because each perspective maps naturally to the business model. Retention (customer) drives ARR (financial). Developer capability (learning and growth) drives deployment speed (internal processes).

Healthcare

A hospital or health network might use:

- Financial: Achieve cost per episode below benchmark; maintain operating margin at 3%

- Customer (Patient): Patient satisfaction score above 90%; readmission rate below 8%

- Internal Processes: Average patient wait time under 20 minutes; infection rate below 1.5%

- Learning and Growth: 95% staff compliance with mandatory training; nursing turnover below 12%

Healthcare is actually where the BSC found some of its strongest adoption in the public sector. The multi-perspective approach maps well to the complexity of delivering care, where financial sustainability and patient outcomes are both non-negotiable.

Manufacturing

A manufacturing business might look like:

- Financial: Reduce cost of goods sold by 10%; improve EBITDA margin to 18%

- Customer: On-time delivery rate above 97%; defect rate below 0.5%

- Internal Processes: Equipment utilisation above 85%; reduce rework hours by 20%

- Learning and Growth: Cross-train 60% of floor staff on secondary skills; reduce workplace incidents to zero

Manufacturing BSCs tend to be operationally heavy. The internal processes perspective often gets the most detail, which makes sense — operational efficiency is the main competitive lever.

Government / Non-Profit

- Financial: Stay within approved budget; reduce per-citizen service cost by 5%

- Customer (Stakeholder): Community satisfaction above 75%; service response time under 48 hours

- Internal Processes: Process 90% of applications within legislated timeframes

- Learning and Growth: Fill 80% of vacancies from internal promotions; increase digitally delivered services to 70%

Government BSCs often rename the 'financial' perspective to something like 'stewardship' since profit isn't the goal — responsible use of public resources is. The framework is flexible enough to accommodate this.

Balanced Scorecard vs OKRs: What's the difference?

Here's the conversation that comes up in every strategy team at some point: should we use a Balanced Scorecard, or OKRs?

They're not identical tools, and the differences matter.

The BSC is comprehensive and structured. It's designed for whole-of-organisation visibility — linking your operational activities to your strategic objectives across four dimensions. It tends to be updated quarterly or annually. It works best when the strategy is relatively stable and you need a way to communicate it across a large, complex organisation.

OKRs are lighter and faster. An Objective is a qualitative direction. Key Results are measurable outcomes that tell you whether you got there. OKRs are set every quarter, reviewed weekly, and owned by teams and individuals — not just the executive team.

The practical differences:

Neither is universally better. The BSC is stronger for organisations that need comprehensive strategic reporting across many stakeholders. OKRs vs KPIs is a separate question worth understanding too — since both the BSC and OKRs use KPIs, but in different ways.

When to use a Balanced Scorecard (and when not to)

The BSC is a good fit when:

- You're a large, complex organisation that needs to report strategy across divisions

- You have relatively stable strategic priorities that don't change every quarter

- You need to communicate strategy to a broad stakeholder base (board, executives, regulators)

- You're in a sector (healthcare, government, manufacturing) where the four perspectives map naturally to your operating model

The BSC is a harder fit when:

- Your team is small and the overhead of maintaining four perspectives isn't worth it

- Your strategy changes frequently and you need something more agile

- You want day-to-day execution to be connected to strategy, not just tracked quarterly

- You're building a culture of accountability and ownership from the team level up

Many companies run both: a BSC at the corporate level for board reporting, and OKRs at the team level for execution. That's a reasonable approach — as long as the two don't contradict each other.

Getting started with Balanced Scorecards

If you're evaluating the Balanced Scorecard as a framework, the best place to start is a simple test:

Can you write one sentence for each of the four perspectives that describes what success looks like for your organisation this year?

If you can, you probably have enough clarity to build a BSC. If you can't, you might need to do some strategy work before the framework can help you.

If your main challenge is bridging the gap between strategy and execution — making sure your team's daily work is actually moving toward your goals — that's a different problem. It's the problem OKRs were designed for.

.png)

.jpg)